IRS Notices

IRS CP14 Notice: What It Means, Your Deadline, and What to Do in 2026

The short answer: a CP14 notice is the IRS's first bill for unpaid tax — not an audit. It shows the tax year, the balance with penalties and interest, and a pay-by date, typically 21 days from the notice date. Pay or set up a payment arrangement by that date and the collection sequence stops before it starts.

You filed months ago and moved on. Now there's a plain white envelope from the Department of the Treasury on your counter saying you owe money you didn't budget for — with penalty and interest lines you've never seen and a deadline a few weeks out. That knot in your stomach is normal. Here's the part that matters: the CP14 is the earliest, cheapest, most fixable moment in the entire IRS collection process, and every option on the menu is still open to you.

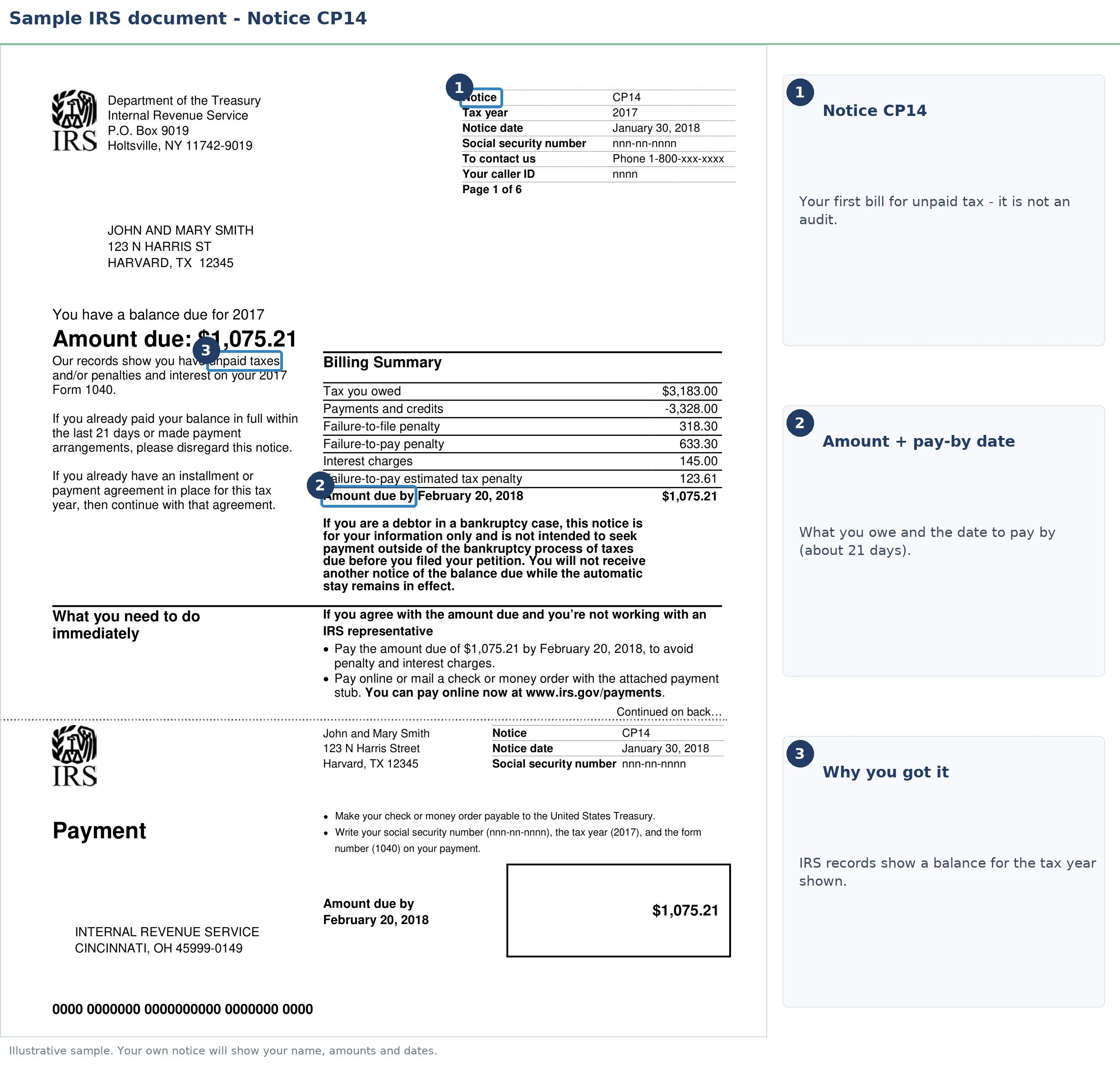

This guide covers what the notice means, exactly how long you have, what each ignored week costs, and every realistic path if you can't pay in full. The image below shows what a genuine CP14 looks like and where to find the two numbers that control everything — the notice date and the total amount due.

⏱ Your deadline: You typically have 21 days from the date on a CP14 before the IRS escalates. (If you owe $100,000 or more, the window shrinks to 10 business days.) The date that legally controls is the pay-by date printed on your notice — after it passes, the 0.5% monthly late-payment penalty and daily interest keep compounding and the next notice queues up automatically.

Why you got a CP14 notice

A CP14 means the IRS processed a tax return under your Social Security number and its records show a balance due. It is the first — and mildest — letter in the collection sequence. Nearly every CP14 traces back to one of three causes:

- You filed but didn't pay in full. The most common trigger, especially for anyone with 1099 income and no withholding — the return was accurate, but the money wasn't there in April.

- You paid, but the payment didn't land where you expected. Payments cross in the mail with the notice, get applied to the wrong tax year, or post to the wrong spouse's account. If you're sure you paid, start with our guide to a CP14 notice but I already paid.

- Penalties and interest were added to a balance you thought was settled — the tax line matches your return, but the total is higher than anything you recognize.

The notice itself breaks the total into tax, penalties, and interest, line by line, for one specific tax year. If you received several IRS letters at once, or you're not sure this one is even a bill, our decoder on why did I get a letter from the IRS maps every notice type — this page covers only the CP14.

Two things a CP14 is not: it's not an audit (nobody is questioning your deductions), and it's not a levy (nothing is being taken). It's a bill. And in 2026, it's usually a machine-generated one — the IRS mails millions of CP14s in the weeks after each filing season, with no human review before yours went out.

First: confirm the CP14 is actually right

A meaningful share of CP14s are wrong, already paid, or aimed at the wrong year — so verify before you pay a dollar. Ten minutes of checking:

- Log in to your IRS online account and compare the balance shown there against the notice. A payment made in the last few weeks may already have posted, making the notice moot.

- Match the notice to your return. Same tax year? Same tax figure? If the tax matches but the total is higher, the difference is penalties and interest — a different problem with different fixes.

- Check where your payment went. Electronic payments applied to the wrong year are a classic CP14 cause. If the amount itself looks off, see our guide to a CP14 wrong amount.

- Screen for scams. A real CP14 arrives by postal mail — never email, text, or social media. Real payments go only to the United States Treasury or through IRS.gov. Anyone demanding gift cards, wire transfers, or payment apps is a criminal, not the IRS.

If the notice is wrong, respond in writing with proof — never pay a balance you don't owe on the theory the IRS will sort it out later. Refunding a double payment takes far longer than disputing the bill.

What a CP14 costs you each month you wait

An unpaid CP14 balance grows by a 0.5% failure-to-pay penalty every month, plus interest that compounds daily at the federal rate. The penalty caps at 25% of the tax, but interest never caps — it runs until the balance is zero.

One piece of good news hides in that math: because you filed, you avoided the failure-to-file penalty, which at 5% per month is ten times larger than the late-payment penalty. The expensive mistake is already behind you; what's left is a carrying cost you can shut off.

To see your own numbers, you can estimate the accrual with our IRS penalty and interest calculator — it estimates how the monthly penalty and daily interest stack on your specific balance.

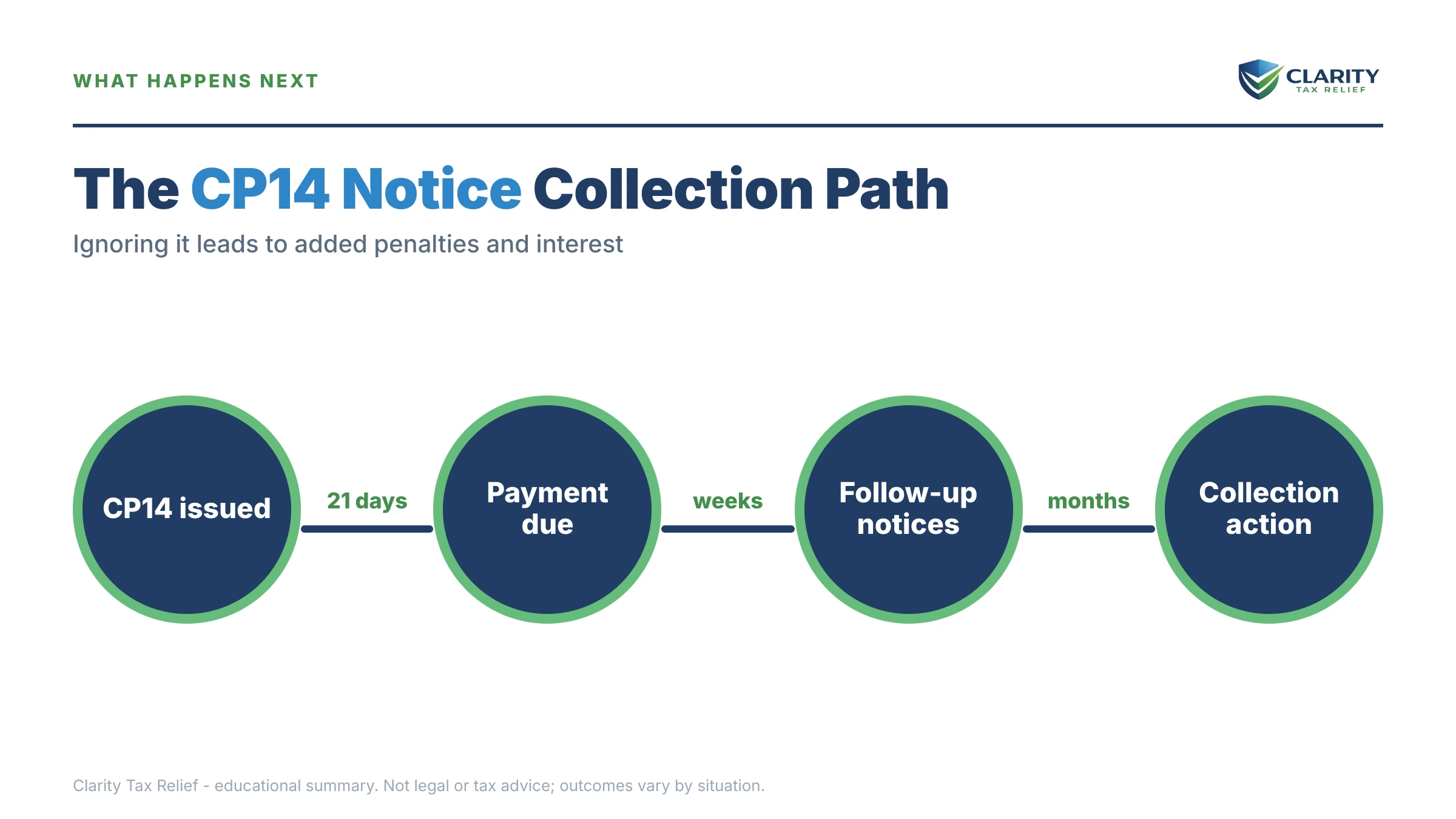

What happens if you ignore a CP14 notice

Ignoring a CP14 starts an automated notice sequence that ends with the legal power to garnish wages and take money from bank accounts. No human decides to escalate your file — the system does it on a schedule, with the notices typically arriving about five weeks apart:

- CP14 — first bill. You are here. No enforcement power exists at this stage; every option is still open and cheap.

- CP501, then CP503 — reminder notices. Still just bills, but the balance has grown each month and the tone sharpens.

- CP504 notice — Notice of Intent to Levy. The IRS can now seize your state tax refund under IRC §6331(d), and a federal tax lien becomes a live possibility. This one arrives by certified mail.

- LT11 notice / Letter 1058 — final notice of intent to levy. A 30-day clock starts, along with your Collection Due Process appeal rights (requested on Form 12153). After those 30 days, the IRS can garnish wages and levy bank accounts.

- Levy. A wage garnishment is continuous — it repeats every paycheck until released. A bank levy freezes funds for a 21-day hold, then the money leaves.

If you rent, don't assume you're insulated because there's no house to put a lien on. For renters, the paycheck and the bank account are the first targets — the two assets a levy reaches fastest. And for balances that grow past $66,000 (the 2026 threshold), the IRS can also certify the debt to the State Department, blocking passport renewal.

One 2026 reality makes this sequence more dangerous, not less: the IRS workforce was cut roughly 27% in 2025, so reaching a human to fix a problem is harder than ever — but the automated systems that issue these notices, liens, and levies never stopped. The machine escalates whether or not anyone ever reads your file.

| Stage | What it adds | Your window |

|---|---|---|

| CP14 | First bill; no enforcement power yet | Typically 21 days from the notice date |

| CP501 / CP503 | Reminders; balance grows monthly | The pay-by date printed on each notice |

| CP504 | State tax refund can be seized (IRC §6331(d)); lien risk rises | The deadline printed on the notice |

| LT11 / Letter 1058 | Final notice; full levy power pending; CDP appeal rights | 30 days to request a hearing on Form 12153 |

| Levy | Continuous wage garnishment; bank levy with 21-day hold | Release requires action — waiting doesn't end it |

Holding a CP14 right now?

Your notice has a printed pay-by date — typically 21 days from the notice date. Get your CP14 reviewed free before that window closes: an experienced tax professional will verify the balance, decode your options, and map the cheapest way out. No pressure, no obligation.

Your options if you can't pay the CP14 in full

The IRS has five real resolution paths behind a CP14, and every one of them stops the escalation sequence — the notice just doesn't advertise them. If this is your exact situation, we also have a dedicated walkthrough for when you've got a CP14 and can't pay. The options:

- Pay in full. If you can, do it by the pay-by date — that ends penalties, interest, and the notice sequence in one move. Direct Pay from a bank account is free; cards carry processor fees. Our CP14 pay online walkthrough shows each method click by click.

- Short-term payment plan — up to 180 days. $0 setup fee. Penalties and interest continue, but the collection sequence stops. Best when the money is coming (a bonus, a tax refund, a sale) and just isn't here yet.

- Installment agreement — a monthly plan. Owe $10,000 or less? The guaranteed installment agreement means the IRS must accept your plan if you've stayed compliant and can pay within three years. Owe up to $25,000 — or up to $50,000 with direct debit? The streamlined installment agreement requires no financial disclosure, and combined balances of $50,000 or less can be set up online over as long as 72 months (or by mail on Form 9465).

- Currently Not Collectible status. If paying anything would leave you unable to cover rent, food, or utilities, IRS Currently Not Collectible status pauses collection entirely while your finances recover. The debt remains and interest accrues, but levies and garnishments stop.

- Offer in Compromise. Settling for less than you owe is real but means-tested — the IRS accepted roughly 1 in 5 offers in FY2024, and approval depends entirely on whether your income and assets genuinely can't cover the debt. There's a $205 application fee and a 20% down payment on lump-sum offers, both waived with low-income certification (AGI at or below 250% of the poverty line). Read how does an offer in compromise work before assuming this is your path.

- Penalty relief — often stackable with any option above. If you've been penalty-free for the prior three years, first-time penalty abatement can remove the failure-to-pay penalty in a single request. Starting this summer, the IRS's new Automatic Exemption from Penalty (AEP) begins applying that relief automatically, no request needed — but for a CP14 in hand today, ask rather than wait. Reasonable cause (illness, disaster, circumstances beyond your control) is a separate path if your history isn't clean.

| Option | Who typically qualifies | Cost & terms |

|---|---|---|

| Short-term plan (180 days) | Most individuals who can full-pay within 6 months | $0 setup; penalties and interest continue |

| Guaranteed installment agreement | Balance ≤ $10,000, compliant filing history | Must full-pay within 3 years; IRS must accept |

| Streamlined / online installment agreement | ≤ $25,000 (≤ $50,000 with direct debit); ≤ $50,000 combined for online setup | Up to 72 months; setup fee applies (lowest online with direct debit); no financials |

| Currently Not Collectible | Documented hardship — paying would prevent basic living expenses | $0; collection paused; debt and interest remain |

| Offer in Compromise | Means-tested: income + assets genuinely below the balance | $205 fee + 20% down on lump-sum (both waived with low-income certification) |

| Penalty abatement (FTA / AEP) | Clean penalty history for prior 3 years, or reasonable cause | Free to request; removes penalties, not tax or interest |

A worked example: say you owe $4,800

Say you're a renter with a W-2 job and rideshare income on the side, and the CP14 says you owe $4,800 for last year because nothing was withheld from the side income. Here's the honest math on each path (hypothetical figures, before daily interest):

- Do nothing: the failure-to-pay penalty alone runs 0.5% × $4,800 = $24 every month, capping at $1,200 — and interest compounds on top of the whole pile while the notices escalate beneath you.

- 180-day short-term plan: roughly $800/month for six months, $0 setup. The penalty shrinks as the balance falls — around $70–$85 in total penalty over the six months, plus interest. Cheapest total cost if your budget can absorb it.

- Guaranteed installment agreement (36 months): $4,800 ÷ 36 ≈ $134/month before accruals. Because the balance is under $10,000, the IRS must accept this if you've stayed compliant.

- 72-month plan: $4,800 ÷ 72 ≈ $67/month before accruals — the gentlest monthly hit, but the most total interest, since accrual runs the whole six years.

- An Offer in Compromise? Honestly, rarely the right tool at this size: with a steady paycheck, the IRS's own collection math will usually show it can collect $4,800 in full over time. Chasing an offer here typically costs more than it saves.

And if your real fear is a levy on your paycheck or bank account: at the CP14 stage, that power does not exist yet. A levy requires the LT11 final notice plus 30 days — several notices and many weeks away. Any plan you start today makes it never happen.

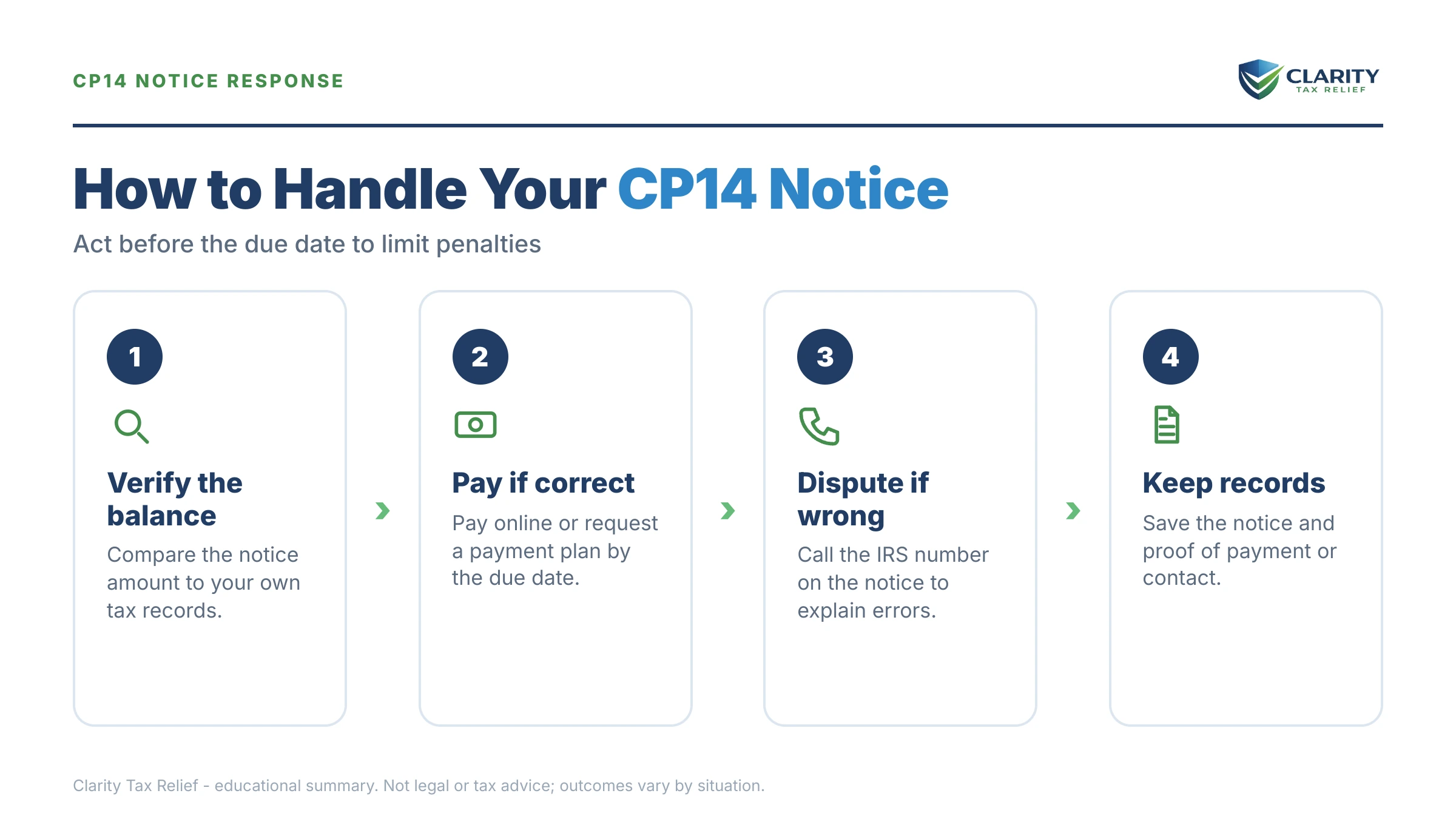

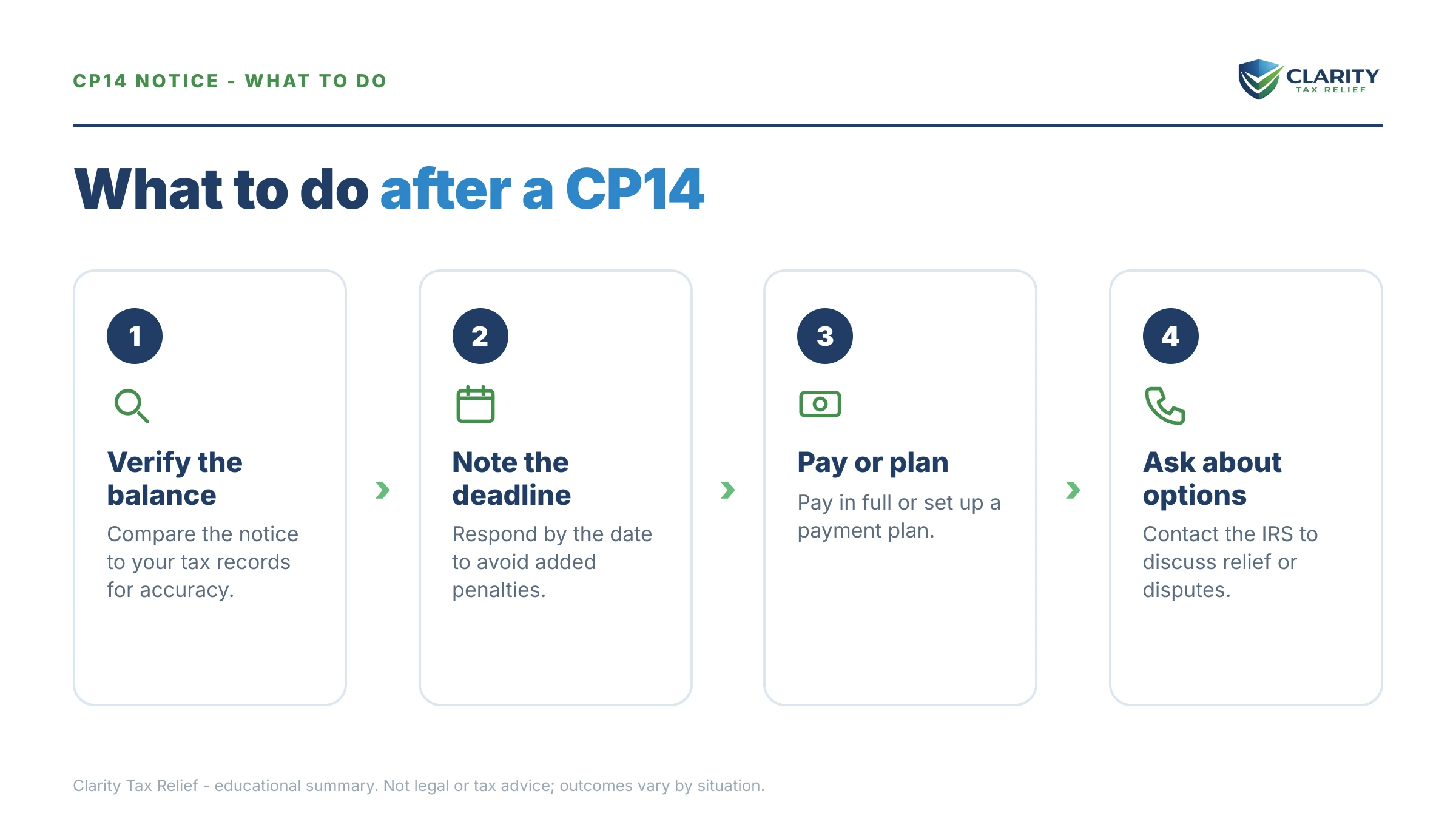

How to respond to a CP14 notice, step by step

- Verify the balance. Log in to your IRS online account and compare the balance there with the amount printed on your CP14 before you pay anything.

- Find your deadline. Locate the notice date and the pay-by date on page one — the pay-by date is the clock every other decision runs on.

- Pay in full if you can. Pay by the printed date through IRS Direct Pay from your bank account, which stops the failure-to-pay penalty from growing and ends the notice sequence.

- Set up a resolution if you can't pay. Choose a short-term plan, an installment agreement, hardship status, or an offer before the pay-by date — any accepted arrangement stops the escalation to CP501, CP503, and CP504.

- Dispute in writing if the notice is wrong. Send proof of payment or corrected figures to the address on the notice, keep copies of everything, and follow up through your online account.

- Request penalty relief. If you've been compliant for the past three years, ask for first-time abatement of the failure-to-pay penalty — it can often be granted in one phone call or letter.

Situations that change the answer

The right CP14 response shifts with your circumstances — these are the ones that most often change the play:

- Married filing jointly: both spouses are fully liable for the entire balance, no matter whose income created it. A divorce decree assigning the debt to your ex doesn't bind the IRS — only the two of you.

- Self-employed or 1099: fix the cause, not just the bill. Without quarterly estimated payments going forward, resolving this CP14 just books your spot in the CP14 notice 2027 wave for this year's income.

- Multiple years owed: each year generates its own CP14, but one installment agreement can — and should — cover every assessed balance. The thresholds above apply to your combined total, which is why a second year can push you out of the easy online tiers.

- You dispute the amount: don't set up a plan on a number you believe is wrong — an agreement can read as acceptance. Dispute first, with documents, then resolve whatever survives.

- Genuine hardship or fixed income: if any payment would break your budget, Currently Not Collectible status exists precisely for you — don't sign up for a plan you'll default on.

- Business balance: the business version of this bill is the CP161, which follows its own sequence — and payroll-tax balances escalate far faster than individual income tax.

- State taxes: a CP14 is federal only. If you also owe your state, expect a separate bill on a separate clock — states run their own statutes and programs, and some collect more aggressively than the IRS.

What a CP14 looks like on your IRS transcript

Your account transcript tells the same story as the CP14 in code form — useful for confirming the notice is real and seeing exactly how the balance was built. The codes you'll typically find behind a CP14:

| Code | What it means | What to do |

|---|---|---|

| 150 | Your return posted and the tax was assessed | Confirm the amount matches the return you filed |

| 276 | Failure-to-pay penalty charged | Check first-time abatement eligibility — this line can often be erased |

| 196 | Interest charged to the account | Accrues until paid; it drops only as the balance drops |

| 971 | Notice issued — this entry is your CP14 going out | Match its date to the notice date; that started your clock |

| 826 | A refund from another year was applied to this balance | Verify the CP14 total reflects the credit before paying |

When you can handle a CP14 yourself — and when help changes the outcome

Most CP14 recipients do not need professional help, and anyone who tells you otherwise is selling. Handle it yourself when:

- You agree with the balance and can pay in full or within 180 days — pay online, done;

- You owe under $25,000 for a single year and just need a simple monthly plan — the online agreement takes about 15 minutes;

- Your only issue is the penalty and your prior three years are clean — a first-time abatement request is one call or letter.

Experienced help genuinely changes outcomes when the CP14 sits on top of something bigger: multiple years owed or unfiled (the order you fix things in changes what you pay), a balance you dispute with prior-year complications, business or payroll tax in the mix, a hardship case that needs the financial statement built correctly the first time, or Offer in Compromise math where one wrong figure sinks the application. If a later notice — CP504 or LT11 — has already arrived alongside the CP14, the clock is genuinely short and a professional review should come first. And if you can't get through to the IRS at all and a deadline is bearing down, the Taxpayer Advocate Service is a free, independent option inside the IRS itself.

Terms on your CP14, decoded

- Notice date: the date printed at the top right — every deadline on the notice counts from it, not from the day you opened the envelope.

- Balance due: the total of tax, penalties, and interest as of the notice date; it keeps growing daily after that date.

- Failure-to-pay penalty: 0.5% of the unpaid tax per month, capped at 25% — the line penalty abatement can erase.

- Interest: a statutory charge that compounds daily at a rate adjusted quarterly; it can't be waived just because you asked, only reduced by paying the balance down.

- Levy vs. lien: a levy takes (wages, bank funds); a lien claims (a public legal interest in what you own). Neither exists at the CP14 stage.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause that clock.

The IRS's own page, Understanding your CP14 notice, is worth a read alongside this guide — it's the primary source for the notice's layout and payment instructions.

If your CP14 sits on top of a messier picture — unfiled years, a balance you dispute, a later notice already in the stack — a free case review at (888) 825-7779 or through the 2-minute form can map the right order to fix it in.

CP14 questions, answered

Is a CP14 notice serious?

A CP14 is serious but very fixable — it's the first notice in the IRS collection sequence, and no enforcement power exists at this stage. The IRS cannot levy your wages or bank account from a CP14 alone. The real danger is ignoring it: the 0.5% monthly failure-to-pay penalty and daily interest keep growing, and the notices that follow — CP504, then LT11 — carry genuine levy power.

How long do I have to respond to a CP14 notice?

You typically have 21 days from the date printed on the CP14 before interest and penalty terms tighten and the next notice queues up; if you owe $100,000 or more, the window is 10 business days. The date that legally controls is the pay-by date printed on your specific notice — always go by that. Missing it doesn't trigger a levy, but it does restart the automated escalation clock.

What if I can't pay the amount on my CP14?

You have more options than the notice advertises: a short-term plan giving you up to 180 days with no setup fee, a monthly installment agreement (up to 72 months online for combined balances of $50,000 or less), Currently Not Collectible status if paying would cause genuine hardship, or an Offer in Compromise when the IRS's own math shows you can't pay in full. Any accepted arrangement stops the notice sequence, though interest continues until the balance hits zero.

I already paid — why did I get a CP14?

CP14s regularly cross in the mail with recent payments, and some are applied to the wrong tax year or wrong spouse's account. Log in to your IRS online account and check whether your payment posted to the year shown on the notice. If it did, the notice may already be moot; if the notice is simply wrong, respond with proof of payment rather than paying twice — the IRS will not reliably catch its own error.

Does a CP14 mean I'm being audited?

No — a CP14 is a bill, not an audit. It means the IRS processed your return and its records show a balance due, usually from tax you reported but didn't fully pay, plus penalties and interest. Nobody is questioning your deductions or income. Audits arrive through entirely different letters, and an underreporting inquiry comes as a CP2000, not a CP14.

Can the IRS levy my bank account or wages after a CP14?

Not from a CP14 alone. Before levying wages or a bank account, the IRS must send a final notice of intent to levy — the LT11 or Letter 1058 — and then wait 30 days while you can request a Collection Due Process hearing. Even then, a bank levy comes with a 21-day hold before funds leave. The CP14 is several notices and many weeks away from that point, which is exactly why acting now is cheaper.

Will a CP14 notice affect my credit score?

No — the IRS does not report tax debt to the credit bureaus, and federal tax liens were removed from consumer credit reports years ago. The indirect risks come later: a filed lien is still a public record that mortgage lenders can find, and an unresolved balance can complicate underwriting. Resolving the CP14 now keeps the debt entirely off that path.

Can I set up a payment plan online after a CP14?

Yes — if your combined balance is $50,000 or less, you can set up a long-term installment agreement online in about 15 minutes, spread over up to 72 months, with no financial disclosure required. If you can pay everything within 180 days, the short-term plan has a $0 setup fee. Setting either one up before your pay-by date stops the notice sequence immediately.

Does interest stop once I'm on a payment plan?

No — interest and the late-payment penalty continue to accrue on the unpaid balance until it reaches zero, even on an approved installment agreement. What the plan stops is enforcement: no CP504, no levy notices, no garnishment while you stay current. That's why the cheapest plan is always the fastest one you can genuinely afford, and why penalty abatement is worth requesting alongside any plan.

Your next 24 hours

- Find the two dates on page one of your CP14 — the notice date and the pay-by date — and put the pay-by date on your calendar. Everything runs on that clock.

- Gather three things: the notice itself, your filed return for the year it names, and any payment confirmations — then verify the balance at IRS.gov/payments through your online account.

- Get a free CP14 case review before the 21-day window on your notice closes — call (888) 825-7779 or use the 2-minute form. Ten minutes now beats untangling a CP504 later.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.